When shopping for life insurance, many people feel overwhelmed by all the different options available. One of the most common questions seniors ask is:

“Should I choose final expense insurance or traditional life insurance?”

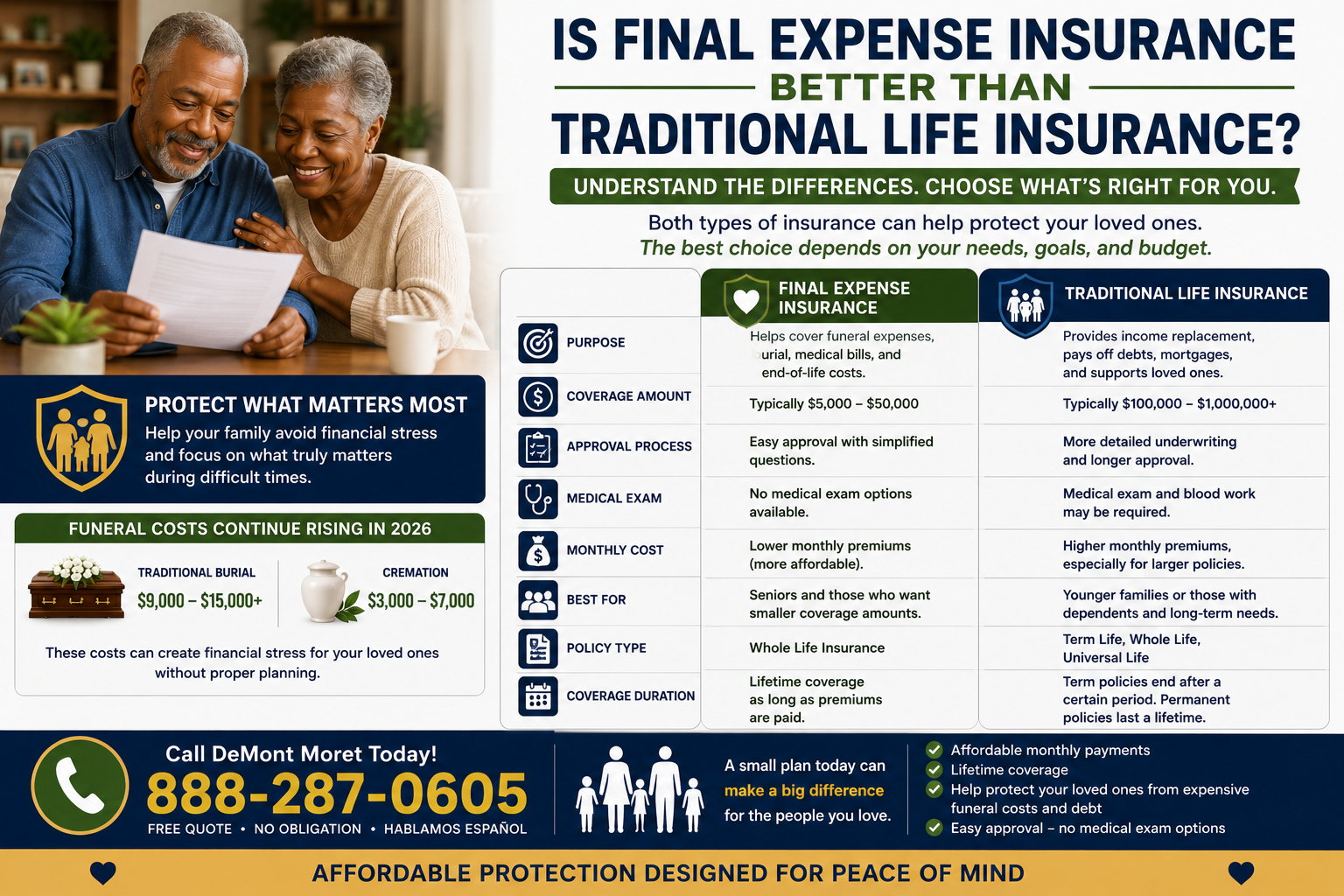

The answer depends on your age, financial goals, health, and the type of protection you want for your family.

In 2026, final expense insurance has become increasingly popular among seniors because it offers affordable coverage designed specifically for funeral costs and end-of-life expenses.

This guide explains the differences between final expense insurance and traditional life insurance so you can better understand which option may fit your needs.

Quick Answer

Final expense insurance is often better for:

- Seniors

- Smaller coverage needs

- Funeral and burial expenses

- Easier approval

- Affordable monthly payments

Traditional life insurance is often better for:

- Income replacement

- Larger coverage amounts

- Younger families with dependents

- Long-term financial planning

Many seniors choose final expense insurance because it is simpler and easier to qualify for.

Call DeMont Moret at 888-287-0605 for help finding affordable coverage that fits your needs.

What Is Final Expense Insurance?

Final expense insurance is a type of whole life insurance designed specifically to help cover:

- Funeral expenses

- Burial costs

- Cremation

- Medical bills

- End-of-life expenses

Coverage amounts commonly range between:

👉 $5,000–$50,000

These policies are especially popular among seniors because they often provide:

✅ Lifetime coverage

✅ Affordable monthly payments

✅ No medical exam options

✅ Easy approval

What Is Traditional Life Insurance?

Traditional life insurance usually focuses on:

- Income replacement

- Mortgage protection

- Family financial security

- Long-term financial planning

Coverage amounts are often much larger.

Policies may include:

- Term life insurance

- Whole life insurance

- Universal life insurance

Traditional policies can provide:

👉 Hundreds of thousands or even millions in coverage

Main Difference #1: Coverage Amount

Final Expense Insurance

Typically:

👉 $5,000–$50,000

Designed primarily for:

- Funeral expenses

- Medical bills

- Small debts

Traditional Life Insurance

Often:

👉 $100,000–$1,000,000+

Designed for:

- Replacing income

- Paying off mortgages

- Supporting children or dependents

Main Difference #2: Approval Process

Final Expense Insurance

Many policies:

✅ Require no medical exam

✅ Use simplified health questions

✅ Offer easier approval

This makes it attractive for seniors and people with health conditions.

Traditional Life Insurance

Traditional policies may require:

- Medical exams

- Blood work

- Detailed underwriting

- Longer approval times

Health conditions can sometimes make approval more difficult.

Call DeMont Moret at 888-287-0605 to explore easy approval final expense options today.

Main Difference #3: Monthly Cost

Final Expense Insurance

Smaller coverage amounts usually mean:

👉 Lower monthly premiums

Example:

- $10,000 policy: approximately $40–$70 per month

- $15,000 policy: approximately $60–$100 per month

Traditional Life Insurance

Larger policies often cost more, especially:

- Whole life insurance

- Permanent coverage plans

Costs depend heavily on:

- Age

- Health

- Coverage amount

Main Difference #4: Purpose of Coverage

Final Expense Insurance

Designed mainly to help families cover:

- Funeral expenses

- Burial or cremation costs

- Medical bills

- Small debts

Traditional Life Insurance

Designed more for:

- Long-term family financial support

- Income replacement

- Mortgage payoff

- Wealth transfer

Why Many Seniors Prefer Final Expense Insurance

Many seniors no longer need massive life insurance policies because:

- Children are grown

- Mortgages may be paid off

- Retirement income is fixed

Instead, many simply want:

✅ Affordable coverage

✅ Peace of mind

✅ Protection for funeral expenses

✅ Easier approval

Final expense insurance provides a simple solution for those goals.

Real-Life Example

Senior Couple

A retired couple mainly wants coverage to help protect each other from:

- Funeral expenses

- Medical bills

- End-of-life costs

They choose:

👉 $15,000 final expense policies

because they are affordable and easy to qualify for.

Younger Family

A younger family with children and a mortgage may choose:

👉 $500,000 traditional life insurance policy

to replace income and protect long-term financial needs.

Funeral Costs Continue Rising in 2026

One reason final expense insurance continues growing in popularity is because funeral costs remain expensive.

Average Funeral Costs:

- Traditional burial: $9,000–$15,000+

- Cremation: $3,000–$7,000

Without planning ahead, these costs often become financial burdens for loved ones.

FAQ

Is final expense insurance worth it?

For many seniors, yes. It helps cover funeral expenses and reduce financial stress for loved ones.

Does final expense insurance require a medical exam?

Many policies offer no medical exam options.

Is traditional life insurance better?

It depends on your financial goals and coverage needs.

Can seniors with health conditions qualify for final expense insurance?

Many seniors with common health concerns still qualify.

How much final expense coverage do most people buy?

Many choose between $10,000 and $25,000 depending on family needs and funeral preferences.

Final Thoughts

Both final expense insurance and traditional life insurance can provide valuable financial protection. The best option depends on your personal goals, age, health, and budget.

For many seniors, final expense insurance offers a simple, affordable way to help protect loved ones from funeral expenses and financial stress.

Planning ahead today can provide peace of mind for tomorrow.